April 1, 2023

Rising Input Costs, Falling Commodity Prices to Squeeze Producer Margins in 2023

Volume 17, Issue 4

April 2023

Rising Input Costs, Falling Commodity Prices to Squeeze Producer Margins in 2023

Written by Dr. Bob Maltsbarger, Senior Research Economist, Food and Agricultural Policy Research Institute

The cost of producing agricultural commodities in 2022 was defined by higher input prices across the United States, regardless of production enterprise. Farmers experienced rapidly rising costs on everything from fertilizer and machinery, to feed and fuel.

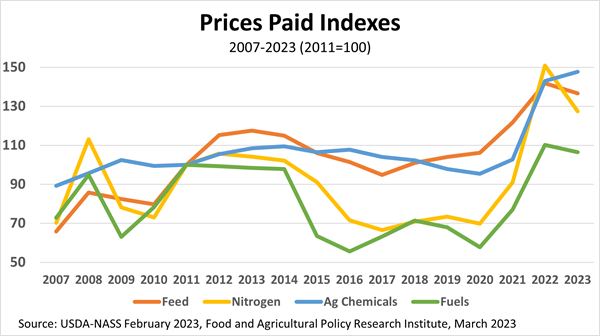

To provide indicators of prices paid by farmers for the production of goods and services, Prices Paid Indexes (PPI) are used; these measures of farmer costs are reported by the National Agricultural Statistical Service (NASS) of the U.S. Department of Agriculture (USDA). These PPIs indicate that, for multiple inputs, the steep rise in production costs began in 2021. The accumulation of these increases is reflected by NASS in its aggregate PPI for Commodities and Services, Interest, Taxes and Wage Rates (PPITW), which increased by 8% in 2021 following a slight decline of 0.1% in 2020.

In 2021, fertilizers and fuels led the climb in cost; these categories increased more than 33% that year. Following their ascent were increases to farm machinery, building materials and feed costs – each increasing 15% or more year-on-year. The rise in 2021 was partially attributed to pandemic-related supply chain issues; however, for inputs like feed and fertilizers, inclement weather and trade conflicts were also problematic.

In 2022, the PPITW increased another 13% with widespread hikes across many input categories. Most PPIs rose to levels not seen since 2008 and several indices hit record highs. Four cost categories that had the steepest increases were fertilizers, fuels, chemicals and feeds. Fertilizers, specifically nitrogen fertilizers, had one of the largest increases over the last two years, increasing 96% from 2020. Across the fertilizer complex, market disruptions like pandemic-related supply chain issues, labor concerns, natural disasters, trade conflicts, increasing crop prices and Europe’s natural gas availability contributed to the rise in cost. Given these challenges, nitrogen fertilizer prices hit a record in April 2022, 26% higher than the prior record set in September 2008.

Chemical costs also showed significant increases over the last two years. After declining in 2020, the chemicals PPI increased 8% in 2021 and another 39% in 2022. Last spring, it was reported that numerous farmers were faced with the choice of changing brands or shifting their herbicide prescriptions after select wholesalers received less than their desired allocations of herbicides such as glyphosate and glufosinate. The reduced chemical allocations were blamed largely on supply chain issues as Bayer declared a “force majeure” event in February 2022, which directly impacted their supply contracts.

The energy sector also contributed to the increase in costs. The fuels PPI experienced a 15% decline in 2020, its lowest point in four years as COVID-19 lockdowns impacted transportation fuel demand. Following this drop, a recovery in transportation fuel demand pushed the PPI up 33% in 2021 and another 43% in 2022, in concert with war influences. Following the initial Russian invasion of Ukraine in early 2022, the monthly fuels PPI climbed 30% through March and April. After this spike in fuel prices, the monthly PPI peaked in June when it exceeded the prior record set in July 2008. Following the peak, fuel prices declined through September but remained elevated until eventually declining in December to close out 2022.

Feed expenses account for the largest single cash expense affecting U.S. farm income, and over the last decade, this category’s share of cash expenses at the national level has averaged more than the sum of fertilizer, chemicals and fuels. The most recent driver of U.S. feed costs has been the ongoing impact of severe and exceptional droughts, especially across the Plains states where drought effects reduced or even eliminated grazing and hay production. Given the continued impact of an extended La Nina, some states faced back-to-back drought conditions in 2021 and 2022. These conditions, combined with weather-related increases in grain, oilseeds and forage prices, drove the feed PPI 15% higher in 2021 and 17% higher in 2022.

Looking at 2023, news on input costs is mixed. Given that numerous PPIs have declined from their 2022 peaks, some farmers may be able to price select inputs at a lower cost this year.

In its March 2023 baseline release, the Food and Agricultural Policy Analysis Research Institute (FAPRI) projects multiple PPIs to decline in 2023. It projects fertilizer PPI to decrease by 12%, feeds by 2% and fuels by 3%. An issue of concern is that despite these declines, most farmers will still be faced with higher combined farm costs in 2023. PPIs offer a reflection of spot prices, but they are not a directly proportional representation for an operation’s cost of production. A large influence on the cost of production for an individual farm is the timing of purchased inputs.

In 2023, the challenge for farmers is three-fold. First, although many input prices are declining, some will continue to rise, such as taxes, interest and wage rates. Second, a declining price may still translate into higher costs. For example, the cost to fill on-farm diesel tanks was higher in January 2023 compared to January 2022. This translates to a cost increase for that farm, even though the price has fallen from its mid-2022 peak. Third, assuming average weather and trend yields, FAPRI projects average farm prices for grains, oilseeds, and select animal and animal product categories to decline in 2023. Given the combination of historically elevated costs and declining output prices, farmers are likely to face a squeeze on operation margins, making the timing of input purchases even more critical this year than in the recent past.

Bob Maltsbarger is a Senior Research Economist with the Food and Agricultural Policy Research Institute at the University of Missouri (FAPRI-MU). He holds a PhD in agricultural and applied economics from the University of Missouri and a MS and BS in agricultural economics from the University of Missouri.

Editor: Chris Laughton

Contributors: Bob Maltsbarger and Chris Laughton

View previous editions of the KEP

Farm Credit East Disclaimer: The information provided in this communication/newsletter is not intended to be investment, tax, or legal advice and should not be relied upon by recipients for such purposes. Farm Credit East does not make any representation or warranty regarding the content, and disclaims any responsibility for the information, materials, third-party opinions, and data included in this report. In no event will Farm Credit East be liable for any decision made or actions taken by any person or persons relying on the information contained in this report.

Tags: outlook, cash field, cost of production, economy, expenses

- Share this post on