June 8, 2022

Takeaways from the 2021 Northeast Dairy Farm Summary

Contents

Volume 16, Issue 6

June 2022

Takeaways from the 2021 Northeast Dairy Farm Summary

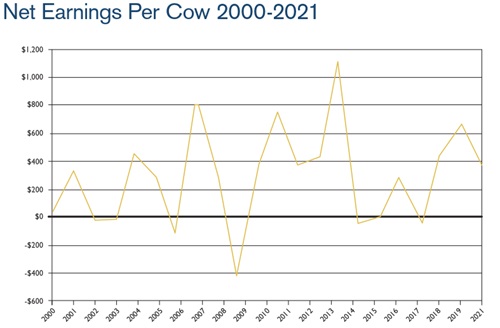

Each spring, Farm Credit East publishes an annual assessment of the economics of dairy in our region, The Northeast Dairy Farm Summary (DFS). 2021 showed moderate average farm earnings of $374 per cow, somewhat greater than the five-year mean of $347. Milk income was greater than in 2020, however overall profitability declined, largely due to a reduction in government payments linked to COVID-19 relief programs.

One of the noteworthy findings of the DFS over the last 20 years is the significant volatility in earnings from year to year, which can be seen in Figure 1:

Source: Farm Credit East

It’s difficult to fully understand 2021 without considering the most unusual year that preceded it. If 2020 was the year when the world was completely disrupted by the COVID-19 pandemic, 2021 was the year when we started to learn to live with it.

While the COVID-19 pandemic had broad and far-reaching impacts, some of the biggest disruptions were felt in the food system. Prior to the pandemic, Americans had been spending just over half of their food dollars outside the home.1 Due to COVID-19-related shutdowns, foodservice demand shrank to nearly zero in the space of just a few weeks in early 2020.

After the initial shock of the shutdown, we began a long, slow, climb back to “normalcy” and with it came some serious supply chain challenges. Processors struggled at times to match product supply and distribution capacity to ever-changing demand, as consumers pivoted first to grocery stores, then gradually back to food away-from-home at restaurants and institutions.

By March of 2021, restaurant sales returned to their pre-pandemic sales volumes. From March through December of last year, restaurant sales surged, exceeding their previous peak levels, due to pent-up consumer demand.2 This was supportive of milk prices, as restaurant demand for dairy products is significant.

Some processors weren’t able to restore capacity fast enough to meet market demands, while others faced logistical challenges. Some cut back on manufacturing shifts because they couldn’t find enough qualified workers to staff them, or because of increased absenteeism. Some co-ops and processors couldn’t get the drivers to haul their products. Exporters struggled to get containers to load for overseas buyers. All of this created tremendous headaches for cooperatives, processors, and exporters. Balancing milk supply with demand has rarely been more challenging than it was in 2021.

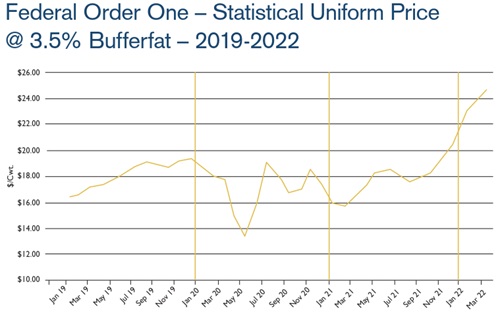

This bumpy road to recovery was reflected in milk prices, as can be seen in Figure 2:

Source: Federal Milk Marketing Order One

The average milk price farmers received in 2021 increased by $0.73 per cwt. compared to the prior year, and the average net cost of production increased by $0.49 per cwt. to $18.60. This increased the profit margin on milk production over 2020, but declines in other income categories, most notably government payments, resulted in lower overall farm profitability. Government payments, which in 2020 were largely related to COVID-19 relief programs, increased from an average of $100 per cow in 2019, to $565 per cow in 2020. They subsequently declined to $201 in 2021.

Average farm earnings in 2021 were $374 per cow compared to $663 in 2020, and $447 in 2019. If we subtract government payments however, those earnings would have been $173 per cow in 2021, $98 in 2020, and $347 in 2019.

A few other observations from the report include that in 2021, farm profitability departed from its usual correlation with herd size. In many prior years farm profitability consistently increased with herd size. However, in 2021, Farms with 99 cows or fewer had average earnings of $258 per cow, those with 100-299 cows had average earnings of $413, 300-699 cows showed the lowest earnings at $131, and farms with 700 cows or more averaged $447/cow. Some of this due to the cost of hired labor on larger farms vs. the lower costs of family labor on smaller farms.

When the sample of farms that participated in the DFS were broken into quartiles by profitability, it’s also notable that all four size groups were represented in each quartile. In fact, the bottom profit quartile’s average herd size was larger than the overall average herd size. While some of this may relate to undervaluing the contribution of family labor, many smaller farms showed strong earnings in 2021. Still, when we looked at the net cost of producing milk, the largest size group (700+ cows) had the edge, with an average NCOP of $18.15/cwt. compared to $18.86/cwt. for the smallest size group (99 cows or fewer).

To access the complete report, visit: FarmCreditEast.com/Reports.

1 USDA Economic Research Service

2 U.S. Census Bureau

Editor: Chris Laughton

Contributors: Tom Cosgrove and Chris Laughton

View previous editions of the KEP

Farm Credit East Disclaimer: The information provided in this communication/newsletter is not intended to be investment, tax, or legal advice and should not be relied upon by recipients for such purposes. Farm Credit East does not make any representation or warranty regarding the content, and disclaims any responsibility for the information, materials, third-party opinions, and data included in this report. In no event will Farm Credit East be liable for any decision made or actions taken by any person or persons relying on the information contained in this report.

Tags: dairy, dairy, dairy, economy

- Share this post on