April 9, 2020

Many businesses are rapidly pursuing the Paycheck Protection Program (PPP) loans because of the amount of immediate cash to offset gaps in short-term cash flow. In addition, many of these loans are expected to be forgiven, resulting in a grant to the business which could be much needed cash flow to assist in surviving what could turn out to be a very difficult year. Here, we discuss areas of opportunity and what it could mean for your business.

Wineries or other similar retail businesses

Many small wineries rely mostly on part-time staff. These staff are not being called in to the winery until the removal of government orders which have partially or fully suspended operations due to limits on travel, commerce or group meetings. Some full-time staff are being laid off or are on reduced hours. Many wineries have had success with curbside sales and online sales. Although wineries are considered essential, most are not able to operate normally since businesses like restaurants and bars are not permitted to open for normal business. For non-essential businesses that must remain closed, the concepts below could be even more relevant.

The efficacy of a PPP loan

A PPP loan that the applicant intends to target “forgiveness” will require 75% of that balance to be spent on funding payroll in 8 weeks from the time of loan closing. In some cases, it will not be to the winery’s advantage to resume full payroll since it’s not the busy season and at least the next 3 to 4 weeks will not allow normal business. In addition, certain generous unemployment rules make it hard to rehire staff without them “losing” money.

The efficacy of Employer Retention Credit

- Applies to businesses that were fully or partially shut down by effects of government orders

- Up to 50% of wages (up to $10,000 of wages per employee, maximum $5,000 credit per employee)

- Can use the credit towards ALL federal payroll taxes, including withheld employee share of taxes

- The credit applies to payroll expenses after 3/12/2020 to 12/31/2020 (a longer period)

- Cannot be paired with the use of a PPP loan

- Can be paired with the deferral of the employer’s share of FICA taxes to be paid ½ in 2021 and ½ in 2022

The usefulness of this credit would apply where a winery has far more part-time staff than full-time and expects to have more payroll costs later in 2020 (after the next 8 to 10 weeks). In this case, the employer can keep cash that would ordinarily have be sent in with payroll reports up to the extent of the accrued credits. (Note: the advantage of PPP increases to the extent you have more annual wages in excess of $24,000).

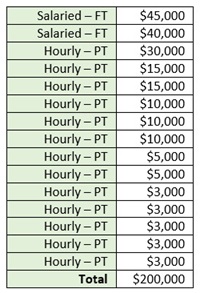

Here's a winery example

Small winery of $220,000 annual payroll with 60% of that occurring between June and December. $85,000 of annual payroll is split between two, full-time salaried individuals. Part time labor hours will be heaviest from July through October.

List of payroll PROJECTED to occur between 3/12/2020 and 12/31/2020:

Employee retention credit allows in this case:

Eight employees over $10,000 = 8 x $5,000 for a $40,000 credit;

In addition, the remainder of part-timers are $25,000 x 50% = $12,500;

so the total available credits are $52,500.

Assuming a simplistic scenario of FICA tax of 15% and minimal federal income tax rate of 10%: payroll obligations could be $50,000.

The credits would allow an infusion of $50,000 of cash into the business - most of which would be in the last half of 2020 (assuming the government orders that suspended normal business operations have not been lifted part way through the year).

In this simplistic example, the PPP loan would be $41,667 (the limit would be approximately 2.5 months of payroll). In addition, some of this loan would likely have to be paid back since it would be forgivable only to the extent the winery could spend 75% of it on payroll in the next eight weeks (not expected). In this case, the credits would exceed the PPP loan and more important the forgivable portion of said loan.

This winery may obtain additional credits through this act or other by:

- Including qualified health plan expenses paid for employees as additional qualifying wages subject however to the same 50% or $5,000 limit.

- Obtaining credits for qualified leave wages under the FFCRA (permissible to use both credits, but not on the same wages).

Concluding thoughts

Although it’s likely that PPP will better serve many winery customers, since it excludes the Employee Retention Credit (ERC), businesses should analyze for themselves which is expected to be better. In addition, most wineries will qualify for the EIDL grant. Some businesses are applying for EIDL on the realty entity and PPP on the operating entity. The purpose of this article is to consider certain small businesses that are unlikely to actually be running full bore in April, May and June, making it difficult to gain the forgiveness of the PPP offer.

To learn more about ERC, click here. For Farm Credit East's recent updates on the ERC, see Employee Retention Credit: Updated Guidance and Tax Implications.

Regional Financial Services Leader

- Share this post on